There’s a deluge of new data and research to wade through every week.

So every Wednesday we’re here to break it all down into digestible chunks: data drop has just the numbers you need to know about, minus the fluff.

This column is sponsored by MobileAction, the premier mobile UA optimization platform.

Contact us to learn how our campaign management and app store marketing intelligence tools can help you generate more downloads efficiently.

Take-Two financials: mobile is 57% of bookings, Toon Blast hits $2bn

Mobile represented 57% of Take-Two’s net bookings by platform ($689.6m) in the three months ended June 30, 2023.

Console was 35% and PC and other were 8%. Total Q124 net bookings were $1.2bn, the higher end of the company’s expectations.

Highlights from the Zynga side of the business were:

- Ad revenue was up 11% YoY, driven by Popcore and new inventory in its portfolio

- Toon Blast hit $2bn in lifetime gross bookings

- Empires & Puzzles “grew quarter-over-quarter”, driven by a new battle pass

- Rollic’s Twisted Tangle hit number one in the US charts on Android

- Social casino games Hit It Rich and Game of Thrones Casino were namechecked as strong performers

- Star Wars Hunters and Socialpoint’s PvP merge game Top Troops are slated for this financial year; the GTA Trilogy remaster is still TBC

- Looking ahead, Take-Two expects full year bookings to be split out as follows: 51% Zynga, 30% 2K, 17% Rockstar Games and 2% other

Playtika’s “constantly searching” for M&A amid mixed financials

Playtika was keen to stress its previous investments in AI during its its Q223 financials.

It also said that after acquiring its Youda Games’ portfolio from Azerion Group for an initial €81.3m ($89.3m), it is now on the lookout for more M&A deals.

Founder and CEO Robert Antokol said:

“We are constantly searching for promising game franchises that we can optimize and monetize, using our operational excellence and best-in-class LiveOps.”

The numbers in brief:

- Playtika generated $642.8m of revenue, down 2.5% YoY

- Credit adjusted EBITDA was $215m, up 6.7% YoY

- Playtika’s direct to consumer revenues hit a new high of $165.3m, up 7.6% YoY. Its direct to consumer business is now 25.7% of overall revenue

- Its casual games portfolio is up 3.7% by revenue YoY, driven by Bingo Blitz, Solitaire Grand Harvest and June’s Journey

- Social casino game revenue declined 9.9% YoY

- Average DAU declined by 12.2% YoY to 8.6m

- ARPDAU increased 12.2% YoY to $0.83

Newzoo estimates global games market value – and Apple and Google’s app store earnings

Newzoo says the entire games market will generate $187.7bn in 2023, up 2.6% YoY.

Mobile accounts for the highest share of that revenue, of course, but Newzoo notes that “a challenging privacy landscape will somewhat limit growth until 2026.”

As above, the research firm estimates a player audience of 3.38bn in 2023, a 6.3+ YoY rise.

The number playing mobile games is believed to be 2.86bn, and the above region-based breakdown suggests that over half of all players worldwide are in the Asia-Pacific region.

In a breakdown of the games market by segment, Newzoo notes that while mobile generates 49% of games industry revenue – $92.6bn – it’s not growing at the speed it once was due to platform privacy policies. It is still fractionally up by 0.8% YoY though:

Console represents 30% with $56.1bn and PC takes up 20% with $37.1bn. There’s also 1% for browser games, a market worth $1.9bn annually.

The split of regions by revenue shows LatAm and MENA growing, and strong demand for console gaming powering growth in North America and Europe:

The relatively low growth for the Asia-Pacific region is mostly down to uncertainty in China, with Newzoo noting restrictions on release licensing and younger players’ game time. The end of the Netease-Blizzard partnership will also dent growth there.

And finally, this top public companies by game revenue list shows the incredible revenue Apple and Google makes from its stores, despite not making or publishing any actual games themselves:

With Apple projected to make $3.68bn annually and Google on $2.43bn, it’s no wonder both companies are keen to maintain their 30% and resist regulatory pressure to open up their stores.

Matchingham Games hits 400m downloads

Hypercasual and quiz game maker Matchingham Games said it has now reached 400m downloads across its portfolio.

Appmagic says the label’s top performers are Braindom 2 (102m lifetime installs), Judgment Day (66m), Braindom (63m), Impossible Date (34m) and Flashback (17m).

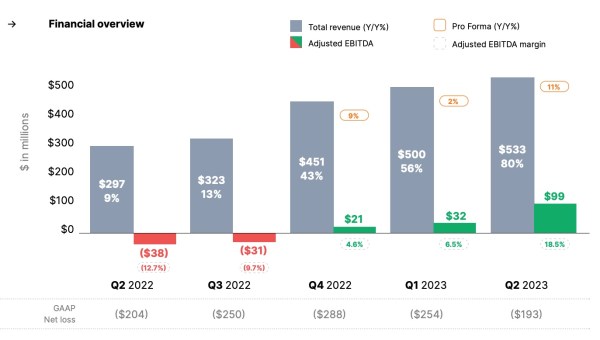

Unity’s merger with IronSource meant a big YoY boost in revenue for the software platform.

Revenue and adjusted EBITDA exceeded guidance as it posted Q223 revenue of $533m, up over 80% YoY.

GAAP net loss was $193m and adjusted EBITDA was $99m, an improvement of $136 million YoY.

Forge of Empires builds to €1bn

InnoGames announced that Forge of Empires has reached €1bn in lifetime revenue.

First released in March 2012, it has 130m registered players and its largest markets by revenue are USA (36%), Germany (19%), France (8%) and UK (4%).

InnoGames also stressed that it was a game with long-term stickiness – a good chunk of its revenue is from users with 3-5 years of play under their belts.